What Would the Board Do?

When a CEO's promises exceed the organization’s capacity by 2,200%, it's not a policy debate—it's a structural crisis

One of the “selling points” for our current president has been his experience as a CEO. I was reading an article in the Washington Post and began to wonder: what would it be like to serve on the board of a company whose CEO had made statements like those discussed in this article?

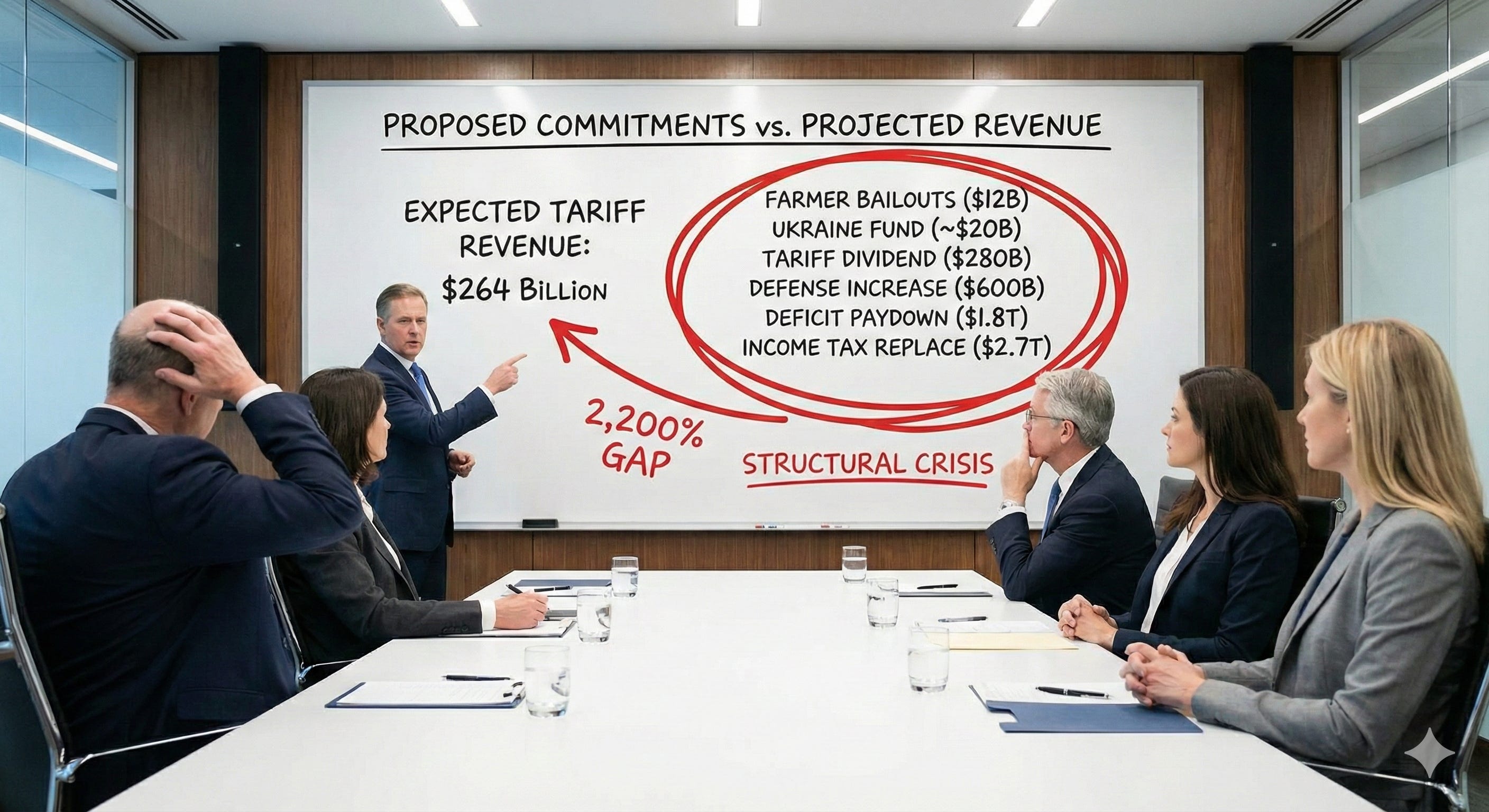

Imagine you’re on the board of a public company. Your CEO walks into the quarterly meeting and announces he’s found a new revenue stream. It will generate $264 million this year.

Then he starts making commitments against it:

- $300,000 for an emergency program

- $1.6 million per year for employee benefits

- $10 million to seed a new investment fund

- $2.5 million in bonuses for a particular division

- $12 million to compensate a supplier group hurt by his own policies

- $20 million for a strategic initiative

So far, so good. That’s $46 million—well within the $264 million. Your CFO is nodding.

Then the CEO keeps going:

- $280 million in dividend payments to shareholders

- $545 million to offset losses from another initiative he championed

- $600 million to fund an expansion he’s calling his “dream project.”

- $1.8 billion to pay down company debt

- $2.7 billion to eliminate a major cost center entirely

The room goes quiet. You do the math. The CEO has just committed to $6 billion in spending against $264 million in revenue.

That’s not a rounding error. That’s a 2,200% gap between promises and capacity.

What do you do?

This Isn’t Hypothetical

The numbers above are real. I’ve just moved the decimal point.

President Trump has promised that tariff revenue will cover nearly $6 trillion in costs. His own Treasury Department projects tariff revenue of $264 billion this year. The Cato Institute has been tracking these promises since the campaign. Added together, Trump has committed the same revenue source to:

- WIC funding during the government shutdown ($0.3B)

- Child care tax credit expansion ($1.6B/year)

- A sovereign wealth fund ($10B in stakes taken so far)

- “Warrior dividend” payments to military members ($2.5B)

- Farmer bailouts for those hurt by tariffs ($12B)

- A “Ukraine victory fund” (~$20B estimated)

- A “tariff dividend” of $2000 per taxpayer(280B)

- Offsetting the deficit increase from the One Big Beautiful Bill Act ($545B)

- Expanding defense spending to 1.5 trillion(600B increase)

- Paying off the deficit ($1.8T)

- Replacing the income tax entirely ($2.7T)

The math doesn’t work. It cannot work. Everyone who looks at it knows it cannot work.

So what happens next?

The Board’s Fiduciary Question

Back to our boardroom. You’re a director. You have legal obligations to shareholders. Your CEO has just made public commitments that are mathematically impossible to honor.

This isn’t a policy disagreement. You might love the CEO’s vision. You might believe tariffs are brilliant strategy. You might agree with every single priority on that list.

None of that matters.

What matters is that your CEO has made binding representations to stakeholders—employees expecting bonuses, divisions expecting funding, shareholders expecting dividends—that cannot all be honored. Most of them cannot be honored at all.

A responsible board asks three questions:

First: Is this an error or a pattern?

An error gets corrected. A pattern reveals something about how the CEO processes reality. When the same revenue source gets promised to a dozen different purposes across a dozen different contexts, you’re not looking at miscalculation. You’re looking at how this person makes commitments.

Second: Does the CEO understand the problem?

This is the harder question. There are only three possibilities:

1. The CEO knows the commitments can’t be honored and is making them anyway (integrity failure)

2. The CEO cannot maintain coherent commitments across contexts (cognitive limitation)

3. The CEO is indifferent to whether commitments can be honored (commitment network collapse)

None of these is acceptable in a fiduciary context. A board doesn’t need to determine which failure mode is operating. Any of them justifies action.

Third: What is our exposure?

Every unfulfilled commitment creates liability. Farmers who planned around promised bailouts. Military members who expected bonus payments. Taxpayers who voted based on promised dividends. Shareholders who priced in promised deficit reduction.

The gap between commitment and capacity doesn’t disappear. It gets distributed—to those who relied on the commitments.

Integrity as Structure

I’ve spent thirty years helping organizations see something they can’t see themselves: their commitment networks.

Every organization runs on commitments. Requests made, promises given, expectations created. Most of these are invisible. They live in conversations, emails, handshakes, policy announcements, and quarterly earnings calls. They form a network—a web of who owes what to whom.

When that network is coherent, the organization executes. Commitments get honored. Trust accumulates. The system works.

When that network is incoherent—when commitments exceed capacity, when the same resource is promised to multiple parties, when no one is reconciling the load—execution fails. It fails predictably. And it fails in ways that damage everyone who relied on the commitments.

This is why I don’t think of integrity as a moral virtue. I think of it as a structural property. Like load-bearing capacity in a building.

You can admire the building’s architecture. You can love its design philosophy. You can believe deeply in what it represents.

But if the load-bearing structure cannot support the weight being placed on it, the building will fail. Not because of values. Because of physics.

The $6 trillion in commitments against $264 billion in revenue isn’t a political position. It’s a structural analysis. The commitment network cannot bear this load.

What Becomes Visible

When you map commitment networks, you see things that participants inside the system cannot see.

You see that the farmer bailout and the tariff dividend are competing for the same dollars. You see that “paying off the deficit” and “replacing the income tax” require the same revenue stream multiple times over. You see that the sovereign wealth fund and the Ukraine victory fund and the dream military are all drawing from a well that’s already dry.

You see that these commitments weren’t made in coordination. They were made in separate contexts—campaign events, Truth Social posts, press conferences, bilateral meetings—without anyone reconciling them into a coherent whole.

This is what commitment network collapse looks like from the inside: each promise makes sense in its moment. The farmer standing before you needs help. The military members deserve recognition. The taxpayers would love a dividend.

The collapse isn’t visible until you step back and see the network.

The Board’s Decision

So what would a responsible board actually do?

Not debate the CEO’s policies. Not argue about whether tariffs are good economics. Not take political positions.

A responsible board would:

Demand reconciliation. Which commitments will be honored? In what order? With what resources? The CEO doesn’t get to keep making promises without saying which earlier promises are being abandoned.

Institute commitment governance. No more public commitments without capacity validation. The CFO signs off before the CEO speaks. This is basic corporate discipline.

Assess fitness for the role. If the CEO cannot or will not operate within the constraint that commitments must be capable of being honored, the CEO cannot serve in a fiduciary capacity. This isn’t punishment. It’s a structural necessity.

Communicate clearly to stakeholders. Those who relied on commitments deserve to know which will be honored and which will not. The longer the ambiguity persists, the greater the damage when it resolves.

The Uncomfortable Truth

We don’t have a board.

The American system places no fiduciary obligation on the President to reconcile public commitments with actual capacity. There is no CFO sign-off requirement. There is no quarterly reconciliation. There is no legal mechanism to demand coherence between promises and resources.

Perhaps it’s a design flaw.

Not a partisan observation—a structural one. Any executive, of any party, can make unlimited commitments against limited resources, and the only accountability is the next election, years away.

The farmers will eventually discover that the bailout competes with the tariff dividend, the defense increase, and deficit reduction. Military members will discover that the warrior dividend was paid from existing appropriations, not from tariff revenue. Taxpayers will discover that replacing income tax revenue with tariff revenue requires tariffs roughly 10 times higher than anyone is proposing.

These discoveries will happen sequentially, in contexts that obscure the pattern. Each broken commitment will be explained individually. The network will remain invisible.

Unless we make it visible.

What Coherence Would Require

I’m not arguing against tariffs. I’m not arguing against any of these priorities. Reasonable people can disagree about all of them.

I’m arguing for coherence. For the basic discipline of not committing the same dollar to twenty-two different purposes.

Coherence would sound like this:

“Tariffs will generate approximately $264 billion this year. Here is exactly how that revenue will be allocated. The farmer bailout is real; these other things will require different funding sources. We will not make commitments we cannot honor.”

That’s not a high bar. It’s the minimum standard we’d expect from any CEO, any CFO, any competent manager of other people’s resources.

The absence of this discipline isn’t a policy choice. It’s a structural failure. And structural failures don’t resolve themselves through debate. They resolve through collapse—and through the damage distributed to those who relied on the structure.

The Question Worth Asking

Here’s what I find myself wondering:

What would it take for us to expect commitment coherence from our leaders the way we expect it from corporate executives?

No agreement with their policies. No approval of their priorities. Just the basic expectation that when they make a commitment, they’ve checked whether they can honor it. That’s when they promise the same revenue to multiple purposes; someone asks them to reconcile. That the gap between promise and capacity gets acknowledged, not obscured.

This isn’t about this President or any President. It’s about whether we have standards for commitment and integrity in public life that match what we demand in private enterprise.

A board would know what to do.

The question is whether we do.